Florida Statute 627.70132 establishes a one-year window for Palm Beach County homeowners to file a claim for storm damage to their roof, and the Florida DBPR's post-storm complaint data consistently shows that the most preventable financial losses occur when homeowners authorize permanent repair work before following the correct sequence. Post-storm roof repair in PBC has a specific legal and insurance sequence that differs from standard repair: documentation precedes protection, protection precedes adjuster inspection, and adjuster inspection precedes permanent repair authorization. Deviating from this sequence in either direction risks both the insurance claim and the physical outcome of the repair.

The Post-Storm Repair Sequence in Florida

Post-storm roof repair in Palm Beach County follows a sequence governed by both Florida insurance law and the practical requirements of a successful insurance claim. Every step must occur in order — skipping or reversing steps compromises the claim.

Types of Storm Damage Requiring Repair vs Full Replacement

Not every post-storm roof condition in PBC requires full replacement. The Florida Building Code Section 706 25% rule determines the threshold: damage affecting less than 25% of the total roof area can be repaired to current code compliance. Damage affecting more than 25% cumulative within 12 months requires full code-compliant replacement. A licensed CCC inspector can assess the extent of damage and provide a written opinion on repair vs replacement — this assessment is separate from the insurance adjuster's estimate and is often worth obtaining independently.

Identifying Storm Damage Types in PBC

Palm Beach County experiences four distinct storm damage patterns that present differently on the roof surface. Knowing which type you have determines the correct repair approach and the documentation you need for the claim.

When to Involve a Public Adjuster

If the insurance adjuster's estimate is more than 20% below the licensed contractor quotes you receive, involving a licensed public adjuster is worth considering. Public adjusters in PBC typically charge 10–15% of the settlement increase they negotiate above the initial offer — meaning they are paid only if they improve the outcome. The Florida Association of Public Insurance Adjusters (FAPIA) at floridapublicadjuster.com maintains a directory of licensed PBC public adjusters. Public adjusters are distinct from attorneys — they do not litigate, they negotiate. See our storm damage claim guide for the full claims process.

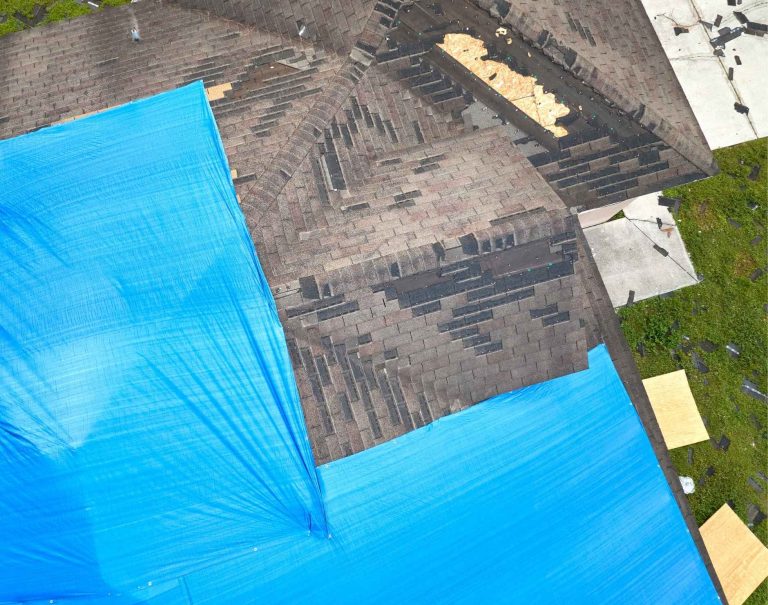

- Document before protecting — photos and video with timestamps before any tarp or emergency work is done

- Download the NWS weather data for your PBC zip code on the storm date — this is your damage causation evidence

- Emergency protection within 24 hours — tarping or membrane to prevent mold (24–48 hour threshold in PBC humidity)

- Notify insurer within 24–48 hours — FL Statute 627.70132, prompt notification required

- Do not authorize permanent repairs before adjuster inspection — this is the most expensive mistake in PBC post-storm repairs

- Get at least 2 CCC contractor quotes after adjuster estimate — compare both to adjuster's repair scope

- If adjuster estimate is 20%+ below contractor quotes — consult a licensed public adjuster (FAPIA directory)

- Pull permit for any repair over $500 — unpermitted post-storm repairs create resale and re-inspection issues