Before You Call Anyone: Document Everything First

Most storm damage roof claims in Florida are weakened — not by the storm — but by homeowners who call a contractor before they call their insurance company. Florida’s claims process rewards documentation above everything else. The homeowner who photographs damage before any emergency work begins has a significantly stronger claim than the homeowner who authorizes tarping first and asks questions later.

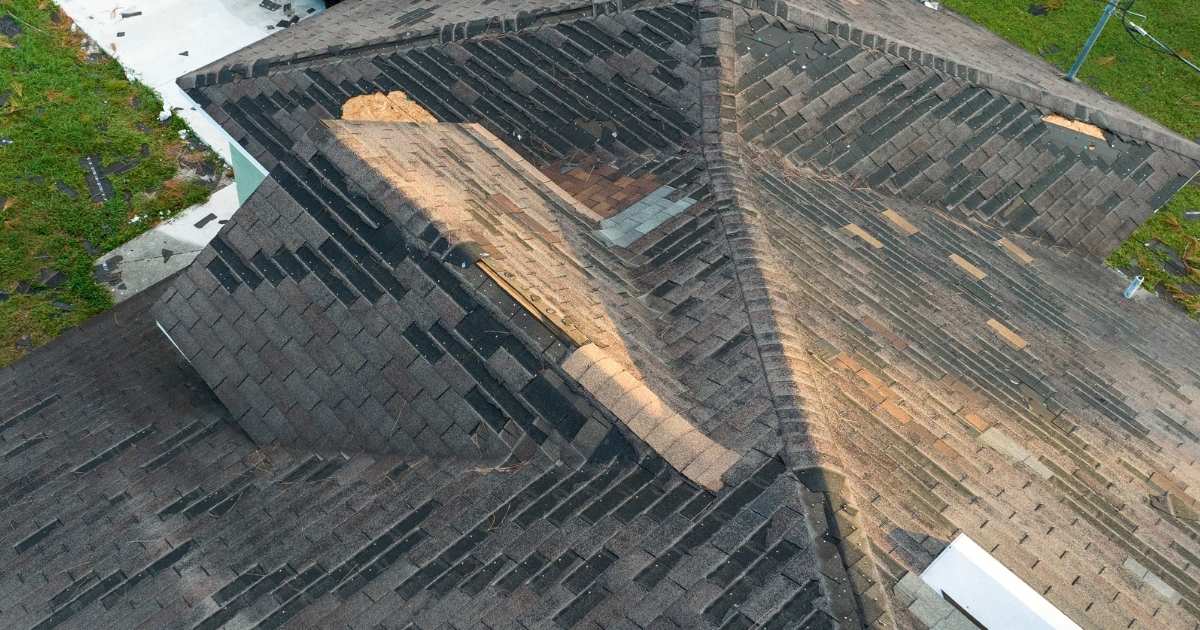

Within 24 hours of the storm passing and conditions becoming safe, photograph every visible area of damage from both the ground and, if accessible, the roof level. Record the date and time stamps on every photo. Open a notes file on your phone and document: the date the storm struck, the NOAA storm name or event if applicable, every affected area you observed, and any interior damage — ceiling stains, wet insulation, damaged drywall — that traces back to a roof breach.

⚠ IMPORTANT — Florida Statute 489.147 prohibits roofing contractors from requiring an Assignment of Benefits (AOB) as a condition of performing emergency repairs. If a contractor presents an AOB document before they’ll tarp your roof, decline it and report them to DBPR at 850-487-1395. Signing an AOB transfers your claim rights to the contractor and removes your ability to manage or dispute your own insurance settlement.

The 7-Step Claims Process for Palm Beach County Homeowners

Step 1 — Document damage before any repairs begin Photograph and video all affected roof areas, gutters, soffits, fascia, and interior ceiling damage. Use timestamped photos. Note the storm name, date, and NOAA event code if available. This pre-repair documentation is the foundation of your claim — insurers use it to establish causation and scope.

Step 2 — File your claim with your insurer immediately Contact your carrier — Citizens Insurance, Universal Property, or your private insurer — and open a claim. In Florida, homeowners have three years from the storm date to file an initial hurricane damage claim under most policies. However, most carrier contracts require “prompt notification,” and waiting more than 30 days substantially increases denial risk. File the same day or the day after the storm.

Step 3 — Authorize emergency tarping — through a licensed CCC contractor only Emergency tarping prevents further water intrusion and is covered under most Florida homeowner policies as a reasonable mitigation expense. A licensed Florida CCC (Certified Roofing Contractor) must perform this work. Verify any contractor’s active CCC license at floridacontractorcheck.com before authorizing any emergency service. Unlicensed contractors — frequently called “storm chasers” — cannot legally tarp or repair roofs in Palm Beach County, and their work will not pass permit inspection.

Step 4 — Receive the insurer’s adjuster inspection Your insurer will assign an adjuster who will schedule an on-site inspection. Be present during this inspection. Your pre-repair documentation gives the adjuster the full pre-mitigation picture. If you believe the adjuster’s damage assessment is incomplete, you have the right to hire a licensed public adjuster to represent your claim independently — this often results in a higher settlement on significant storm damage cases.

Step 5 — Understand the FBC 25% rule before accepting a scope Florida Building Code Section 706 requires that when storm damage plus any prior repairs within 12 months exceeds 25% of the total roof surface area, the entire roof must be brought to current FBC standards. For most properties, this means a full roof replacement — not a patch. Your insurer’s adjuster may initially scope only the damaged area. If the total affected area approaches or exceeds 25%, request a full replacement assessment before accepting any partial settlement.

Step 6 — Select a licensed Palm Beach County roofing contractor Once the insurance scope is agreed, select your contractor independently. You are not required to use any contractor your insurer recommends. Obtain at least two written estimates from licensed CCC contractors active in Palm Beach County. Verify each license at floridacontractorcheck.com. Confirm the contractor will pull a permit — all roofing work in PBC requires a permit, and a completed roof without one is not FBC-compliant and will not qualify for Citizens Insurance wind mitigation credits at resale.

Step 7 — Confirm permit, inspection, and wind mitigation report After work is complete, verify that the permit is closed with a passing final inspection through Palm Beach County’s Building Division. Request a new wind mitigation inspection (OIR-B1-1802 form) immediately after completion. A compliant new roof qualifies for wind mitigation discounts that frequently reduce Citizens Insurance premiums by 20–40% annually — making the updated mitigation report worth requesting on the day the contractor leaves.

Storm Damage Documentation Checklist

Adjusters assess claims faster and more accurately when homeowners provide organized documentation. Prepare this file before the adjuster arrives:

What to have ready for your insurance adjuster:

- Timestamped photos and video of all exterior roof damage, taken before any tarping or repair

- Photos of interior water intrusion — ceiling stains, wet insulation, damaged drywall — with date stamps

- The storm name, date, and NOAA event documentation (download from weather.gov)

- Your policy number and current coverage summary (roof replacement cost vs. ACV)

- Prior roof maintenance records, if available — they demonstrate reasonable upkeep

- Any prior inspection reports or wind mitigation forms (OIR-B1-1802) on file

- Written receipts for any emergency mitigation already performed (tarping, boarding)

- Name, license number, and invoice from any emergency contractor already engaged

Citizens Insurance Roof Claims: What PBC Homeowners Need to Know

Citizens Insurance is the state-backed carrier of last resort and the largest single insurer of residential properties in Palm Beach County. Citizens applies specific claim standards that differ from private market policies in ways that affect storm damage settlements.

Actual Cash Value vs. Replacement Cost Coverage Citizens policies issued after July 1, 2023 under Florida’s insurance reform legislation may pay storm damage claims on an Actual Cash Value (ACV) basis — meaning depreciation is deducted from the payout — unless the homeowner purchased a Replacement Cost Value (RCV) endorsement. Confirm which coverage type your policy carries before your adjuster arrives. ACV settlements on roofs over 10 years old frequently fall short of actual repair costs.

The 25% Rule and Citizens Coverage Scope Citizens applies the FBC 25% rule strictly. If storm damage triggers a full replacement requirement under FBC Section 706, Citizens is obligated to cover the full replacement — not just the storm-damaged area — provided the damage is documented to that threshold. Many homeowners leave money on the table by accepting a partial settlement on a roof that legally required full replacement. A licensed roofing contractor experienced with Citizens claims can identify this threshold before you sign any settlement agreement.

NOTE — Citizens Insurance requires that a valid roof inspection confirm at least three years of remaining useful life to maintain or renew a policy. If your storm-damaged roof is over 20 years old, schedule a condition assessment alongside your claim process — a compliant repair or replacement resets this clock.

Assignment of Benefits and Storm Chasers: The Two Risks That Cost Florida Homeowners Millions

Every major Florida hurricane season brings two specific threats that compound storm damage for homeowners: Assignment of Benefits (AOB) abuse and unlicensed contractor fraud.

Assignment of Benefits (AOB) An AOB is a legal document that transfers your insurance claim rights to a third party — usually a contractor. Florida Statute 489.147, enacted to curb widespread AOB abuse following Hurricane Irma and Hurricane Michael, makes it illegal for contractors to require AOB as a condition of emergency repairs. Despite this, some contractors still present AOB documents during the post-storm window when homeowners are under pressure.

Signing an AOB means the contractor — not you — negotiates directly with your insurer, controls the repair scope, and receives payment. Disputes between the contractor and insurer frequently result in inflated claims, litigation delays, and homeowners left with unresolved repairs. Do not sign an AOB for any roofing work.

Unlicensed Storm Chasers After every significant storm in Palm Beach County, out-of-state contractors arrive soliciting repairs door-to-door. Many hold no Florida CCC license. Work performed by an unlicensed contractor is illegal under Florida Statute 489.127, will not pass Palm Beach County Building Division inspection, does not qualify for Citizens Insurance wind mitigation credits, and creates direct homeowner liability if injuries occur on site. Verify the active CCC license of every contractor before signing any agreement. Search by name or license number at floridacontractorcheck.com — the search takes 30 seconds.

Realistic Claims Timeline for Palm Beach County

Storm damage roof claims in Florida typically resolve in 60–120 days from filing when documentation is complete and no disputes arise.

- Days 1–3: File claim, document damage, authorize emergency tarping with licensed CCC contractor

- Days 5–14: Insurer assigns adjuster; on-site inspection scheduled

- Days 14–30: Adjuster submits assessment; coverage determination issued

- Days 30–45: Negotiate scope if FBC 25% rule triggers full replacement; obtain contractor bids

- Days 45–90: Permit pulled; replacement or repair completed; final inspection passed

- Days 90–120: Final payment issued; wind mitigation inspection completed; Citizens premium adjustment applied

Claims involving disputes over scope — most commonly the 25% rule threshold — extend this timeline by 30–60 additional days. Engaging a licensed storm damage contractor experienced with Citizens Insurance early in the process accelerates the scope agreement phase significantly.

Frequently Asked Questions

How long do I have to file a storm damage roof claim in Florida? Florida law gives homeowners three years from the date of the storm to file an initial claim for hurricane damage. However, Citizens Insurance and many private carriers require prompt notification — delaying your report by more than 30 days substantially increases denial risk for late reporting. File immediately after the storm, even if you haven’t yet assessed the full scope of damage.

Will my Citizens Insurance policy cover a full roof replacement after storm damage? Citizens Insurance applies Florida Building Code Section 706: if storm damage plus any prior repairs in the past 12 months affects more than 25% of the roof surface, the entire roof must be brought to current FBC standards. In most cases that means a full replacement covered under your claim — but only if the damage is documented correctly before any emergency repairs begin and the threshold is properly argued during the adjuster inspection.

What is Assignment of Benefits (AOB) and should I sign it? Assignment of Benefits (AOB) transfers your insurance claim rights to a contractor, allowing them to bill your insurer directly. Florida Statute 489.147 prohibits contractors from requiring AOB as a condition of emergency repairs. Signing an AOB removes your ability to negotiate, dispute, or manage your own claim. Do not sign one. Report any contractor who makes AOB a condition of service to DBPR at 850-487-1395.

Can an unlicensed contractor perform storm damage repairs in Palm Beach County? No. All roofing work in Palm Beach County requires a Florida CCC (Certified Roofing Contractor) license. Work performed without a valid CCC license will not pass permit inspection, will not qualify for Citizens Insurance wind mitigation credits, and creates direct liability for the homeowner. Verify any contractor’s license at floridacontractorcheck.com before signing anything.

What is the difference between ACV and RCV coverage for roof claims? Actual Cash Value (ACV) coverage pays the depreciated value of your roof at the time of the storm. Replacement Cost Value (RCV) coverage pays the full cost to replace the damaged roof at current prices, minus your deductible. On a 15-year-old roof, ACV coverage may pay 40–50% less than RCV. Review your policy type before a storm occurs — changing from ACV to RCV is far easier before a claim than during one.